Selling Option Premium

About Options

Options, by definition, are a wasting asset. Many first-time option investors learn this fact the hard way by watching their option contracts expire worthless. It is frustrating to have a call option expire on a Friday afternoon only to see the market rally through your strike price the following Monday or Tuesday. The vast majority of options expire worthless; most estimates are somewhere north of 85%.

For some traders, buying options is similar in philosophy to playing the lottery. These traders buy an option for a few hundred dollars and hope for a dramatic price movement that will generate thousands of dollars in profits. While these type of profits can occur, it is very unusual and infrequent. Statistically speaking, the delta of an option tells you the probability that it will expire in the money. A long call option with a delta of 15% will expire worthless 85% of the time. Again, most “cheap” options expire worthless.

Risk Potential

Given that the vast majority (85%+) of long option positions are worthless at the time of expiration, some traders decide that they will sell options and collect the premium. At first, this sounds like an easy way to make money. However, the trading pits are littered with short option traders that “blew up” on a major move. How do you think the traders who were short puts in the S&P faired when the market crashed in 1987? The Long Term Capital bond fiasco destroyed professional traders who were short bond options – calls on the way up to record highs and puts when prices crashed. After two limit down moves in bonds following the all-time-high move, options that had been worth 1/64 or $15.625 were worth $1000. The lottery ticket trade in options does work once in a while, and it is the option seller that has to pay. Therefore, it is important to remember that unlike buying options–a strategy that has fixed risk and unlimited profit potential–selling options has limited profit potential and unlimited risk. Remember, risk management is absolutely critical when trading short option positions.

Any trades are educational examples only. They do not include commissions and fees.

Managing Risk

Selling option premium is very similar to selling insurance, and the option seller can look to the insurance industry for some ideas on managing risk. Most insurance policies come up for renewal every year without a claim. Then, without warning, the industry experiences a year like 2004 when three hurricanes hit Florida causing billions in losses. However, the insurance companies know that they will occasionally experience considerable losses and they do business accordingly. To reduce risk, many insurers use reinsurance, thus spreading part of their risk with other insurers. In addition, most insurance companies spread their risk across various geographic areas and insurance products. Comparable methods of risk management apply to selling option premium.

Diversification through Exposure across Multiple Commodity Markets

Insurance companies do not write a single type of policy in a single area. Similarly, option sellers should not sell premium in only one futures market. For example, an insurer would not write home insurance policies in San Francisco area only because he is well aware that a single earthquake could put him out of business. For this reason, insurers write policies throughout the country, knowing it is highly unlikely that a natural disaster will occur in multiple areas of the country in the same year.

In the same way, as an option seller, one can reduce the risk of being wiped out by a substantially adverse move in a given market by selling premium in a diversified portfolio of markets. Nevertheless, traders must be careful to be truly diversified. Shorting option premium in the Five-year notes, Ten-year notes, and Thirty-year bonds is not diversified, as these are all interest rate contracts on the longer end of the yield curve. Likewise, selling premium in Crude oil, Heating oil, and Unleaded gas does not provide diversification. Exposure across a wide variety of commodity markets will provide some diversification.

Spreading Risk with Short Option Spreads

Is market diversification enough? Even the most successful option traders are not immune from a potentially disastrous market move when they are short “naked” options. In fact, the futures industry is still reeling from a large fund trader who went millions of dollars in the hole being short S&P 500 puts during the mini crash of 1997. As a result, many clearing firms refuse the business of large naked option sellers, especially those in the stock indexes.

Clearing firms are not in the business of turning away trading volume, but they stay in business by managing risk. Equally, individual traders must be aware of their risks and understand how to effectively manage them. Once again, we can look to the insurance industry as an example. As previously stated, many insurance companies use something called reinsurance to reduce risk. An insurance company determines the amount of capital they are willing to risk on a specific policy or group of policies and then purchases reinsurance to cover any losses above that amount. For example, an insurance company is willing to cover the first $10,000,000 of losses in a specific area, so they buy a reinsurance policy that covers everything above $10,000,000 from a different insurer.

If we change the terms, we have just described a short option spread. If a trader sells a $6.40 soybean call, his risk is unlimited. If he simultaneously buys a $6.60 call, he is only risking the 20-cent difference between the two strike prices. This type of action reduces risk and prevents a catastrophic loss situation. Statistically, the $6.60 call will expire worthless more often than $6.40, leaving many traders to believe that they have “wasted their money” on an option that will likely expire. However, in the event that the soybean market rallies through the $6.60 price, the trader will have the significant benefit of being long soybeans at that price – effectively insulating him from additional bullish price action. Most reinsurance purchases also never payout, yet insurance companies continue the practice because without proper risk management catastrophic losses can put them out of business. The same is true for option traders. Selling spreads will reduce risk and margin requirement allowing for better diversification with less capital.

Selling Naked Options

After having offered some horror stories regarding selling naked options, I will offer some ideas on how to do it. Two general ideas that potential option sellers can consider are directional and non-directional strategies.

Directional Trading Strategy with Short Options

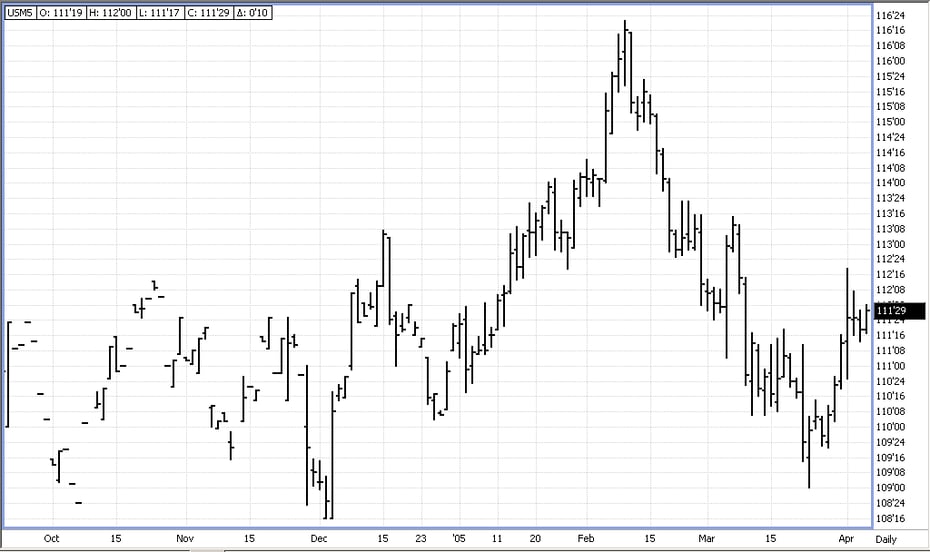

Using a directional trading strategy, a trader would determine his directional bias and pick a trade accordingly. Assume a trader feels that long-term interest rates will rise due to the current economic environment and wishes to enter a bearish trade in the 30-year bond (see bond futures chart, below.) On April 6, 2005 the trader can sell a May 30-year bond 113 call at 15/64. This price is available with the underlying futures contract trading at 111-26. These options have 16 days until expiration. The option seller is looking for the market to settle anywhere below 113. The attractive aspect of this trade is that the trader does not need to be 100% correct in his prediction in order to make money. If, by expiration, the market were to rally one full point in the bonds and settle at 112-26, the 113 call would still expire worthless. If the trader had sold the futures instead of the calls, in this example, the futures trader would have lost $1000 while the option seller collected 15/64 or $234.38. However, there is a downside to this strategy when the trader is correct in their directional opinion. If bond futures fell by two full points prior to expiration, the futures trader would have made $2000 while the option seller would have collected the same $234.38. This strategy is generally best suited for a trader who is willing to accept a long or short position in the underlying market. If a trader is negative on bonds and willing to enter a short futures position, selling the calls may be a viable alternative.

Any trades are educational examples only. They do not include commissions and fees.

Bond Futures Chart

Non-directional Trading Strategy with Short Options

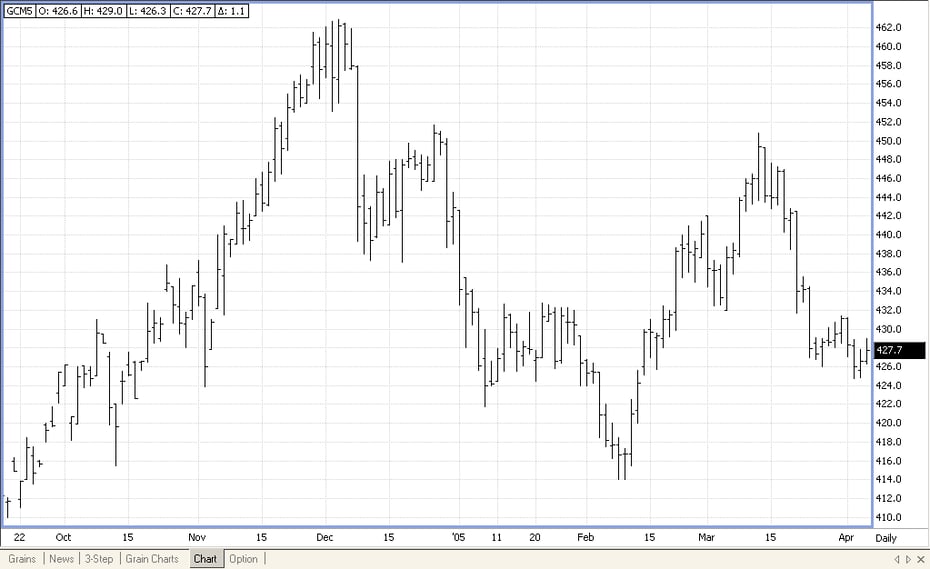

Now, let’s assume our trader is of the opinion that a market is likely to trade in a range. In this case, he may look at a direction neutral option selling strategy. Our trader looks at a gold chart and feels that after the past year’s volatility the market is likely to consolidate and remain in a trading range of $410-$450 (see gold futures chart, below.) He looks at selling the June Gold $450 call and $410 put. The June Gold futures are trading around $427 and the $410-$450 “strangle” is trading at $4.00. At expiration, this strangle gives the trader a break-even range of $406-$454, not including fees. If June Gold futures were trading at $400 at expiration, the short put leg of the trade would be worth $10, resulting in a $6 loss ($10-$4 premium collected=-$6) on the position. This type of trading is often compared to duck hunting. In duck hunting, the hunter uses a shotgun, which sprays the shot over a wide area. A hunter would not use a rifle to hunt for ducks as the rifle projects one small, highly accurate shot. The direction neutral trader looks to establish a position with a wide area in which he can be profitable.

Any trades are educational examples only. They do not include commissions and fees.

Gold Futures Chart

Conclusion

The above ideas are a starting point for the trader looking to become an option premium seller. The option seller can also look at selling implied volatility in delta neutral trades, as well as using ratio and calendar spreads to manage risk while maintaining a short premium position.