Many traders are attracted to options on commodities. They typically prefer the limited risk–premium paid plus commission and fees–and unlimited profit potential features that are exclusive to buying long options outright. The problem with buying options outright, however, is that many traders buy out-of-the-money options because they are less expensive. Statistically speaking, out-of-the-money options will usually expire worthless anywhere from 50%-99% of the time. A long out-of-the-money option can be a great strategy if several things happen and you are near perfect in your timing. For example, if you were to buy a call option, ideal circumstances would allow the underlying market to make a large move higher with an increase in implied volatility the next day. Most traders are not that fortunate when it comes to their market timing. Given the strict circumstances that will allow an outright option purchase to ultimately make a profit, many traders choose to pursue slightly more sophisticated strategies that are inherently more flexible. Option spreads offer a way to trade a directional strategy that will statistically give you a better chance of success for the same dollar risk.

There are more types and combinations of option spreads than we have room to cover in this article. The purpose of this article will be to look at the positive benefits of using “vertical” spreads. Vertical spreads refer to a simultaneous long and short position in options of the same type (both calls or both puts) in the same commodity contracts at different strikes. For example, a long August gold 430 call and a short August gold 450 call would be a vertical call spread. This article will discuss the benefits and costs associated with using these spreads to make directional plays.

Options are a wasting asset. With no change in any of the underlying assumptions, an option will lose part of its value everyday until it expires worthless. Time value only moves in one direction (decreases in value), so as an option buyer one must overcome the effects of time decay everyday in order to make money. Another factor that affects option prices is implied volatility. Implied volatility can increase or decrease. An implied volatility increase will benefit the option buyer and help offset time decay. In addition, movement in the price of the underlying commodity can obviously move either way and benefit or hurt the option buyer. A call buyer will benefit from a rise in the price of the underlying, while the put buyer will benefit from a decline in the price of the underlying.

Traders buy calls in order to take advantage of what they feel will be higher prices in the underlying market. What they generally fail to realize is that not only do they need to be correct in their directional opinion, they also need to be correct in their timing and the direction of implied volatility. A large enough directional move can, however, make up for any volatility or time decay losses.

Typical option buyers see a move in a commodity and feel the move will continue. They look at the option market for an option that costs $500-$2,000 to take advantage of the anticipated large move. The problem with this course of action is two-fold. First, the initial “break out” move likely caused implied volatility to increase. Second, the increase in implied volatility may have forced them to buy an option further out-of-the-money in order to meet their risk/reward objectives.

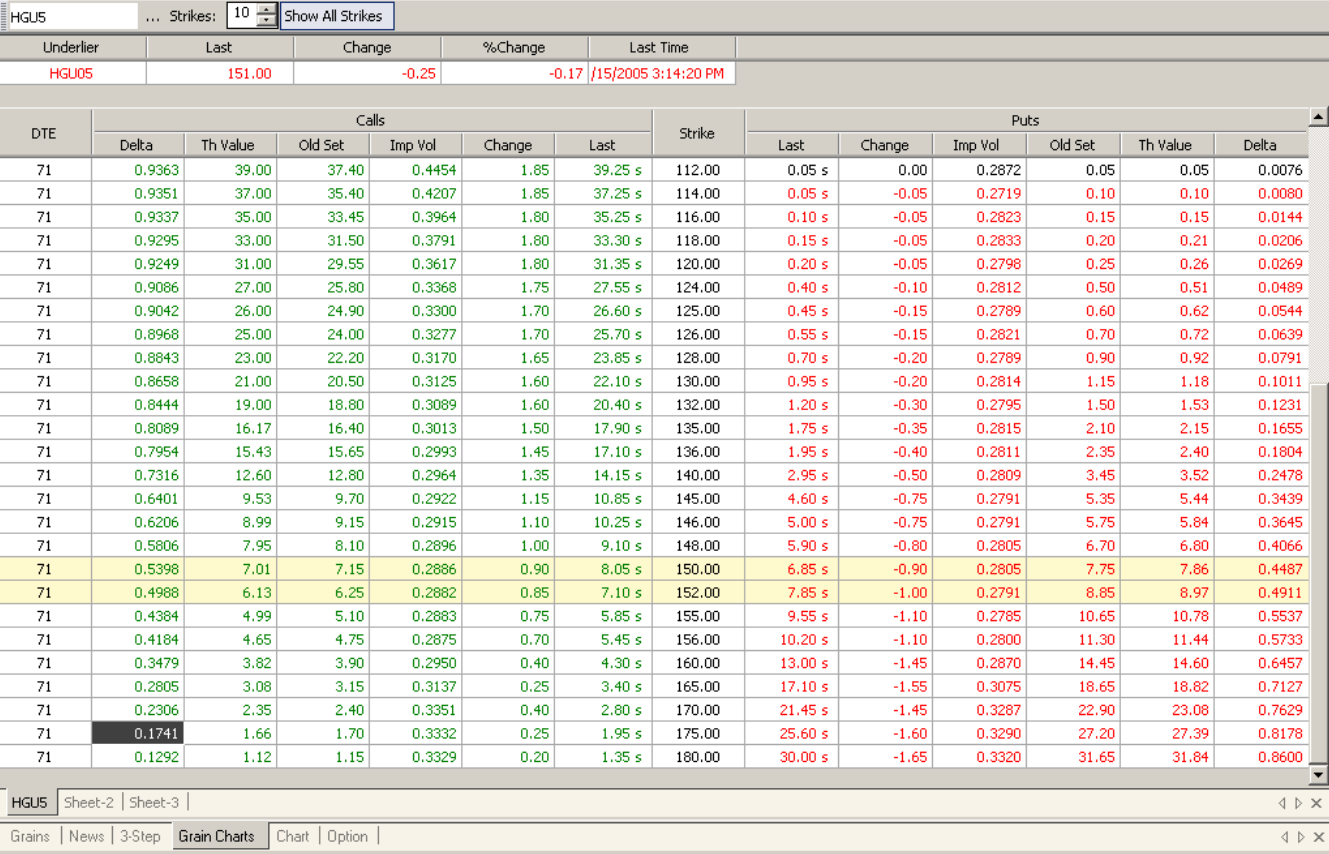

Before we get into our example, we will quickly review the concept of delta. The delta of an option refers to the move an option will make in response to a move in the underlying. At-the-money options will have a delta of 50%. As the option moves further in-the-money, the delta increases and will eventually approach 100%, i.e. the option will act just like a futures contract. As the option moves out-of-the-money, the delta will move toward zero. The delta of an option is also the mathematical probability that the option will expire in the money. For example, an option with a delta of 50 is likely to settle in-the-money half the time.

Any trades are educational examples only. They do not include commissions and fees.

The Copper market has had a solid move higher making new highs. A trader wishes to buy a call for approximately $500 to take advantage of what he views will be higher prices. The at-the-money 152 call settled at 7.10. The delta of the option is 49.88, very near 50. The cost of this option is $1775.00, unfortunately much more than what the trader is looking to spend. If we look at the 175 call, it has a delta of 17.41 and settled at 1.95, or $487.50, a cost within the trader’s parameters. So for $500, the trader can buy an option that is 24 cents out-of-the-money and has less than an 18% chance of settling in-the-money. If we look at a comparable trade in dollar terms using a call spread, we can buy the 152 call for 7.10 and sell the 156 call for 5.45, a difference of 1.65 or $412.50. By definition, the 152 call will expire in-the-money almost 50% of the time.

Any trades are educational examples only. They do not include commissions and fees.

Buying a call spread instead of an outright call does have its disadvantages. Nothing in life is free and call spreads are no exception. By having a further out short call against our nearby long call, we are capping our upside potential. As referenced in the beginning of this article, when you are long an outright option position, you want a rapid and large move in your favor with an increase in implied volatility. Should the market cooperate with that type of move, the outright long option position would perform better, although the call spread would still work.

The factors that hurt a long option holder will logically benefit a trader with a short option position. By using spreads, traders can reduce the effect of negative changes to a long position because they are also holding a short option position. If implied volatility declines, the loss to their long option is partially offset by the gain from the short option. The same holds true for the effects of time decay. The delta of a call spread will be the sum of the two options. In our example, the 152 call delta is 49.88 while the 156 call delta is 41.84. Since we are short the 156 call, the delta on that option is negative. Therefore, the net delta for the 152-156 call spread is +8.04 (49.88 – 41.84 = 8.04). This is approximately half the delta of the outright 175 call and explains why the outright option position will perform better during a rapid and large directional move.

Options are fascinating tools that can be used to create very specific positions tailored to any market opinion. Traders who simply buy calls because they are bullish or buy puts because they are bearish are missing out on many of the benefits of options. Once a trader has a solid understanding of the basics of calls and puts, trading spreads is quite simple. If you are going to trade options, it is advisable to learn about vertical spreads and consider them for your trading activities.